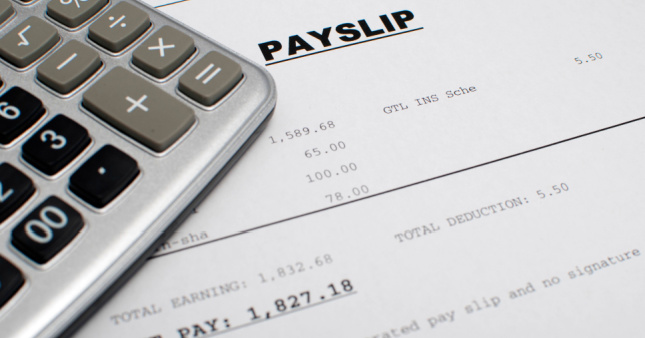

What is gross pay?

When an employee receives a pay slip, it will normally include a figure indicating their ‘gross pay’. Gross pay refers to an employee’s total taxable income for a pay period before any deductions are made.

Income tax, Medicare and Social Security contributions, as well as health insurance, superannuation, and any other deductions are not accounted for when an employee’s gross pay is calculated.

What is the difference between gross pay and net pay?

As well as gross pay, an employee’s ‘net pay’ will also appear on their slip. What’s the difference?

While gross pay shows the amount the employee has earned before any deductions, net pay reflects the amount the employee will receive after deductions are made.

Net pay is almost always a lower figure, reflecting the amount that will be paid into the employee’s bank account. For this reason, net pay is often referred to as ‘take home pay’.

Examples of gross pay and net pay

If an employee’s annual salary is $120,000, then their yearly gross pay is $120,000 and their monthly gross pay is $10,000.

Supposing the same employee paid $29,476 in income tax (calculated based on the current tax rate for this salary), as well as a further $6,524 in superannuation and other contributions, their total deductions will be $35,000.

After these deductions are made from the employee’s gross pay ($120,00 minus $35,000), they will be left with a net pay of $85,000.

What deductions are taken from gross pay?

Mandatory income tax is normally the largest deduction taken from an employee’s gross pay. Australian employers are responsible for deducting tax and sending it to the Australian Taxation Office (ATO).

Anybody who is self-employed needs to calculate their own tax return, set the money aside and pay it directly to the ATO.

It’s also compulsory that employers deduct 2% from an employee’s gross pay for Medicare.

Further deductions may also be agreed on between an employer and employee, including superannuation and health insurance contributions.

Are employers allowed to make deductions?

Employers are legally obligated to make income tax and Medicare deductions from an employee’s pay. Beyond this, an employer can only deduct money if:

The employee agrees in writing and it’s principally for their benefit.

The employee has outstanding court ordered payments.

The deduction is allowed by a law or by the Fair Work Commission.

The deduction is allowed under the employee’s Modern Award.

The deduction is allowed under the employee’s registered agreement, which the employee has signed and agreed to.

An employee’s written agreement must be genuine, and they can’t be forced by an employer into agreeing to any deductions.

it’s important to note that deductions should be shown on the employee’s pay slip, as well as their time and wages records.

Calculating gross pay

If you’re an employee and you want to calculate your gross pay, you can use the information included in your latest pay slip. The calculation you need to make will vary depending on whether you are paid an annual salary or hourly wage.

How to calculate gross pay for an annual salary

The salary recorded in your employment contract will be your official annual gross pay. You can also figure this out by referring to a pay slip. If your pay slip shows a gross monthly pay of $6,000, then you simply multiply this amount by the twelve months of the year (6,000 X 12 = 72,000). Your gross annual pay is $72,000.

Similarly, your annual salary divided by twelve gives you your monthly gross pay.

If you receive any bonuses, financial benefits or commissions, you’ll need to add these too. If you earn $72,000 as a base annual salary, but you’re also paid $5,000 in bonuses for the year, your gross annual pay is $77,000.

How to calculate gross pay for an hourly wage

If you earn an hourly rate of pay and you’re unsure of how many hours you’ll work annually, it’s easiest to wait until the end of the year and calculate it then.

If you work set hours each week, you can calculate your gross annual pay yourself in advance. If you work 20 hours a week at an hourly rate $20, your weekly gross pay is $400, your monthly gross pay is $1,600, and your gross annual pay is $19,200.

Remember – if you take any unpaid days off in the year, you’ll need to deduct the pay from your gross pay. Similarly, if you receive a pay rise or take on any additional shifts, you’ll need to recalculate the rest of the year with the new pay rate or increased number of hours included.

Are you paying your staff fairly?

The Minimum Wage has increased – find out everything you need to know about the latest changes by downloading our FREE Minimum Wage Factsheet.

What is gross salary?

Gross salary refers to the total amount an employer regularly pays to an employee, normally expressed an annual sum that is divided into fortnightly or monthly payments. When an employee starts a new job or receives a pay rise, their gross salary will be agreed upon and laid out in an employment contract.

Much like gross pay, gross salary is an employee’s income before taxes and any other contributions are deducted. Net salary refers to an employee’s take home salary after deductions are made.

Why is gross salary important?

As an employer, it’s vital you have an accurate understanding of each employee’s gross salary. Gross salary is used to calculate the percentage of an employee’s pay you should withhold for taxes, while it can also be used to calculate an employee’s redundancy pay entitlements.

Businesses also rely on gross salary information when budgeting and financial planning. By knowing their total labor costs, employers can allocate financial resources effectively and make informed decisions about expenses, investments, and future growth opportunities.

As an employee, the gross salary an employer offers will be crucial when deciding whether or not to accept a job offer. Gross salary is also important to employees because it is used by creditors when they review loan applications.

What is gross income?

Gross income includes an employee’s gross salary, as well as any:

Tips

Bonuses

Financial benefits

Dividends

Capital gains

Pension payments

Gross annual income refers to all of the above, combined into a yearly sum.

Frequently Asked Questions

What is net income?

Net income is a person’s gross income, minus any deductions. It represents the total amount of money somebody receives in a given period after taxes, interest and other deductions have been made.

If you’re an Australian employer struggling with wages and pay, call our FREE 24/7 Advice Line on 1300 651 415 to get all your questions answered.